Answer: I recently attended a workshop where the chief operations officer of one of the biggest estate companies in South Africa spoke about the double impact of a massive increase in deaths owing to Covid-19 (their numbers were up by 200%) and delays at the Master’s offices, which were closed from time to time because of Covid. Add the complication of your children living overseas and you have the very real prospect of your estate taking a few years to be finalised.

There are a number of things you can do to improve matters:

Attach beneficiaries to investments

Where it makes sense, move some of your investments into structures in which you can attach a beneficiary.

If there is a beneficiary, then the proceeds will be paid out directly to your children and bypass the whole estate liquidation and distribution process.

It will still be deemed an asset and attract estate duty. As it is not dealt with by the executor, however, you will save 4% in executor fees.

Start moving assets offshore

I usually recommend that you have between 40% and 60% of your assets physically offshore. There are two main reasons for this recommendation.

Country risk: If you were living in another country, would you put your assets in South Africa, which accounts for less than 1% of the world’s GDP? We are no longer in the position where we are unable to invest offshore, so it needs to be a conscious decision to keep all your assets here, or to move a portion of them offshore. You reduce the risk of having all your assets in one country.

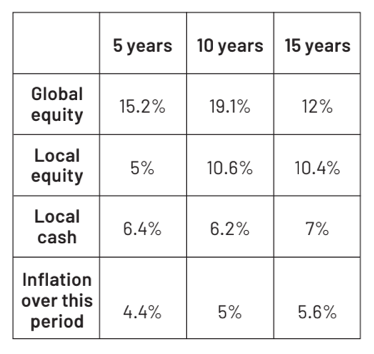

Returns: When converted into rands, global equity investments have outperformed all the major investment classes over five, 10 and 15 years.

Having decent global equities as part of your portfolio should improve your overall returns.

When you move your assets offshore, remember to put them into an appropriate structure. You do not want to create additional problems with probate and situs tax.

Make sure that the structure allows you to attach a beneficiary of ownership to the investment, as this will allow for a seamless takeover of your assets by your children.

I heard a story about someone whose offshore investment was transferred to his children within three weeks of his death, whereas the rest of his estate took two years to be finalised.

How much can you move offshore?

You can easily move R1-million of your assets into an offshore investment. This takes a few days to finalise. You may move an additional R10-million offshore if your income tax affairs are in order. This will take about three weeks to finalise.

Once the money is in an offshore investment, you do not need to bring it back to South Africa.

Should you need some of the money to live on, I usually recommend that my clients bring back six months’ worth of income and keep that in a money-market account to provide them with their living expenses.

Having money offshore can also be useful if you go and live with your children for extended periods. You can use some of the money in this investment to fund your trip and living expenses while overseas. You’re also immunised from any extreme currency movements as your investment is in dollars, pounds or euros.

What can the children do?

Not all investments can have a beneficiary attached, so it does make sense for your children to ensure that they have the necessary documentation in order to inherit.

There are three items that will speed up the inheritance process:

- A barcoded ID;

- A tax number; and

- A South African bank account.

Not having one of these will not be an impediment, but having them will make the inheritance process a lot smoother. I would strongly recommend that they look through their documents and find their ID document and tax number. If they can’t find these, it would be a good idea for them to request a copy of their ID and track down their tax number. These things take time, so it is best that they initiate the process while there are no financial implications to any delay.

A bit of planning now can save a lot of headaches in the future. Start getting the right structures and documents in place now. DM168

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.

Comments - Please login in order to comment.