THE FINANCIAL WELLNESS COACH

Getting to grips with life insurance premium patterns

The impact of age-related increases is really felt in one’s later years when the premiums effectively double every five years.

Question: I recently applied for some life insurance and received a quotation with three different premiums included. My broker suggested I take the highest premium (obviously), while I preferred the lowest one.

The difference between these premiums was something called premium patterns. The highest premium had a fixed compulsory premium of 5%, while the lowest premium had an aggressive age-related premium pattern. What don’t I understand about the choice I need to make here?

Answer: Premium patterns are the annual increases that you will have on your life insurance premiums. The fixed compulsory premium pattern means that your premiums should be increasing by 5% a year. The age-related patterns base the increase on your age at the time of the increase. In other words, the older you get, the bigger your increase in premium will be.

If you are taking out life insurance to cover a short-term risk, such as vehicle finance or a loan, it might make sense for you to choose the lower premium, as it will take a couple of years before the bigger annual premium increases reach the starting premium of the fixed 5% premium.

However, if you intend to have life insurance for the whole of your life, then you should seriously consider choosing the fixed 5% premium increase, or even look at taking a level premium increase, which might be a little higher at inception, but will be more affordable for the rest of your life.

The big increases in premiums really start to take place once you reach your mid-fifties.

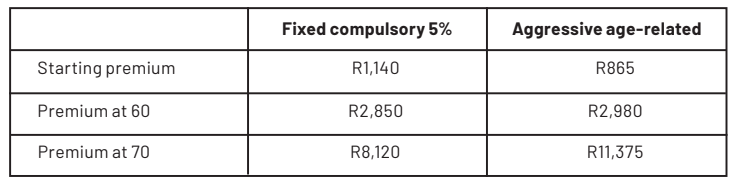

Here is an example of the premium patterns for a 50-year-old:

As you can see, the age-related premiums start off 24% lower and end up being 40% higher once the policy has run for 20 years.

When you take out life insurance, you need to have a clear idea of why you need it. If it is to cover a short-term debt over a five- to eight-year period, then an age-related premium pattern could work. As you can see from the example, the age-related premium was lower for the first 10 years.

If you want the cover for the rest of your life, look at a pattern with a fixed increase or even a payment pattern that is level.

The impact of age-related increases is really felt in one’s later years when the premiums effectively double every five years. Many people cannot afford these increases, which often results in cover being cancelled and liquidity in an estate being lost.

If you find yourself in this situation, get a quote to have the cover reduced and the premium pattern changed to a more affordable level. If this is still unaffordable, you could offer the policy to your children before you cancel it. You can cede the benefits to them and have them pay the premiums. This may be a good investment for them, and when estate liquidity is needed after your death, it could be available in this policy. DM

Kenny Meiring is an independent financial adviser. Contact him on 082 856 0348 or at financialwellnesscoach.co.za. Send your questions to kenny.meiring@sfpadvice.co.za.

This story first appeared in our weekly Daily Maverick 168 newspaper, which is available countrywide for R29.

Comments - Please login in order to comment.