SPONSORED CONTENT

Plotting the long-term drivers of average global inflation conditions

The ongoing debate around the direction of the global interest rate cycle has prompted intense discussions among economists, policymakers, and financial experts globally.

After peaking just short of 9% in 2022, inflation in the United States (US) has come down to just over 3% in the past year. While not quite yet at the Federal Reserve’s target, market participants are looking forward to an environment where lower inflation allows global central banks to ease back on policy tightening.

However, a longer-term perspective reveals some telling themes, which we expect to persist beyond the cycle.

While the drivers of short-run inflation are typically easy to break down into a handful of trends, drivers of longer-term inflation are more important in the setting of average inflation conditions. These are tied to the availability of resources, how efficiently they are utilised, and the demand for investment and spending. On a global scale, efficiencies include optimising the flow of ideas, technology, trade, capital and people between and within different regions.

Analysing the disinflationary drags of the 2010s

A useful exercise when trying to identify these trend drivers, is to look at the key conditions that set the low inflation regime of the 2010s and compare them to today’s environment. Digitisation and automation are set to continue, but the factors that made up the balance of the disinflationary drags of the 2010s have either neutralised or have moved towards being inflationary. The two most material changes we see are declining labour forces – while demand for investment is rising in order to fund the Green Transition – as well as re-shoring, on-shoring and building new supply chains.

Inflation Check-List

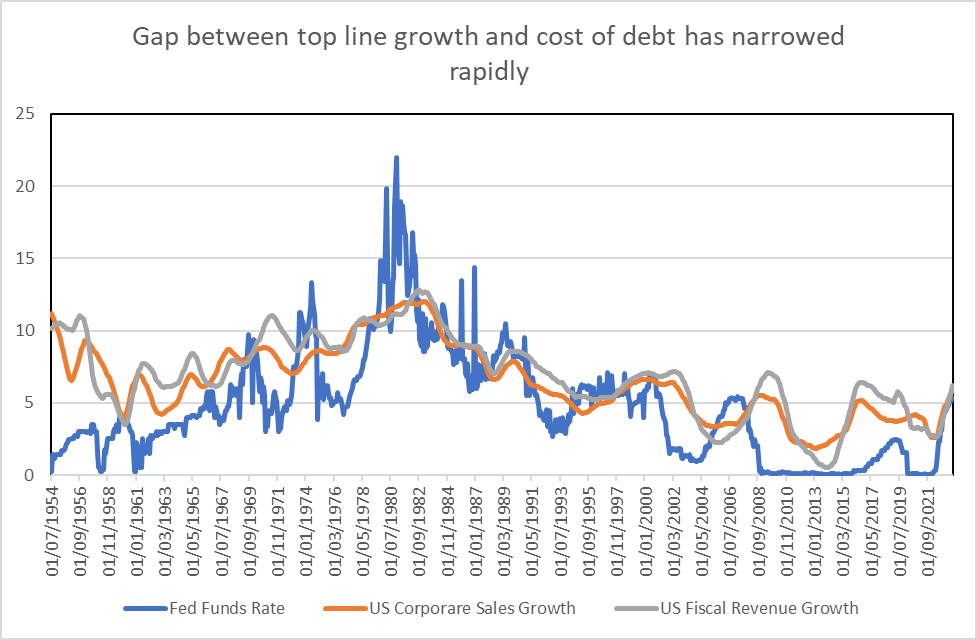

End of an era

The market today remains fixated on the path of potential rate cuts. However, ultimately it is the level of debt and the gap between debt servicing costs and growth that matters most in influencing market dynamics. In the previous decade, interest rates were set close to zero, which was well below growth levels. Simply put, the current environment of higher rates, which has closed this gap, signals an end to the era of zero rates and ‘free carry’.

Source: United States Federal Reserve , US Bureau of Economic Analysis & UC Congressional Budget Office

As such, we expect this narrowing gap between the level of interest rates and growth to:

- Place more pressure on balance sheets and drive debt service ratios higher as cheap, old debt is refinanced to new, expensive debt,

- Detract from corporate margins,

- Force a change in capital allocation decisions,

- Increase pressure on government to raise taxes or find new revenue sources,

- Favour businesses that have front loaded cash flows and benefit from higher interest rates,

- Widen corporate spreads and drive more discretion in risk pricing.

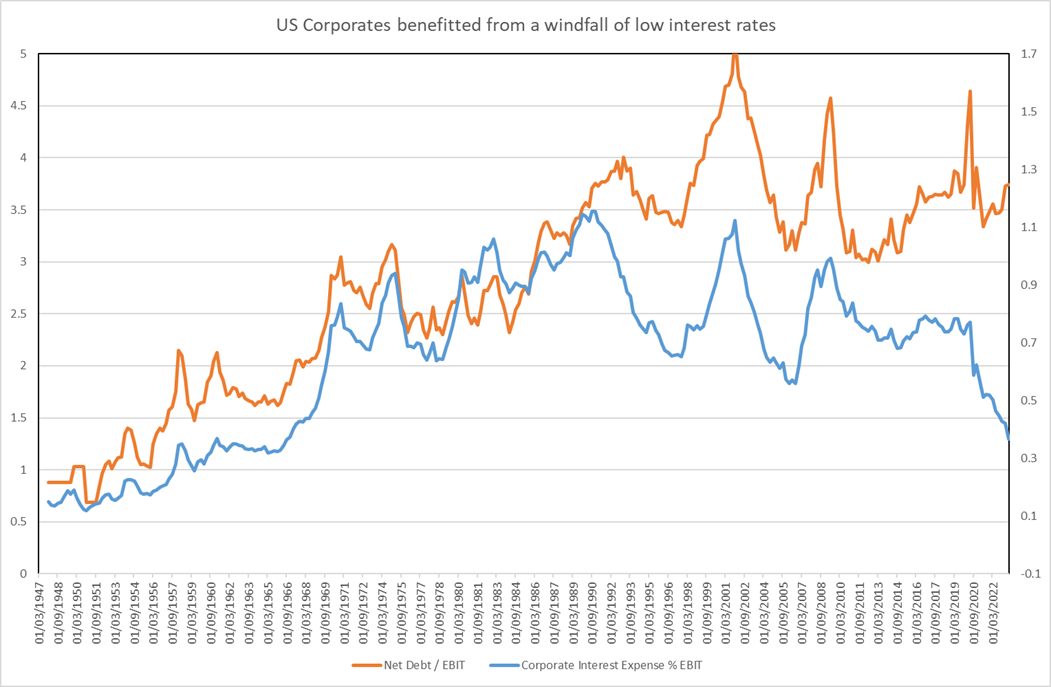

Source: US Bureau of Economic Analysis , MacroSolutions

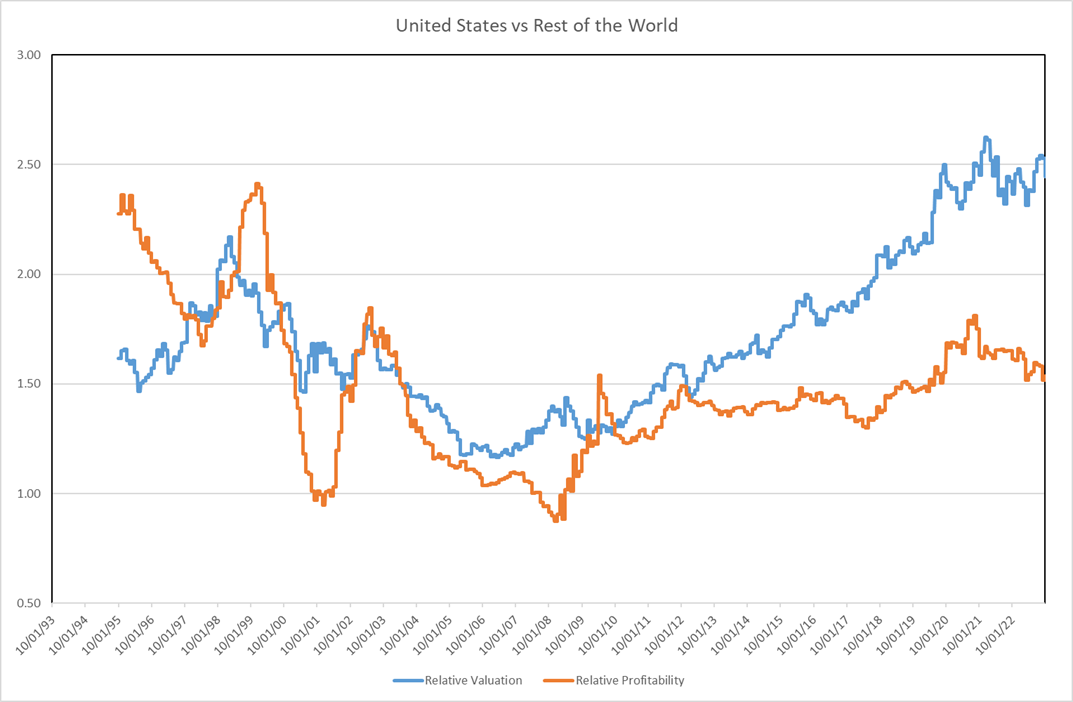

Assessing the alternatives

The low inflation, low interest rate environment during the 2010’s created an ideal setting for growth-oriented companies. Low inflation meant low to no growth for many businesses, while abundant savings reduced the demand for investment and zero rates impaired the income generation of banks in developed markets.

Yet in our current high inflation, high interest rate global environment, there are now alternatives to this, offering growth at reasonable prices for the first time in over a decade.

Many of these opportunities exist outside of the US, and it is in these regions that we see assets priced for perfection. In Japan, for example, the return of inflation, investment and less stringent fiscal handcuffs are boons to economic growth and corporate profits, with financials standing out as significant beneficiaries of higher interest rates. Within emerging markets, we are seeing opportunities from Mexico (with domestic investment set to benefit from US friend-shoring) to the Philippines (a rising middle class, abundant labour and public investment).

Source: MSCI

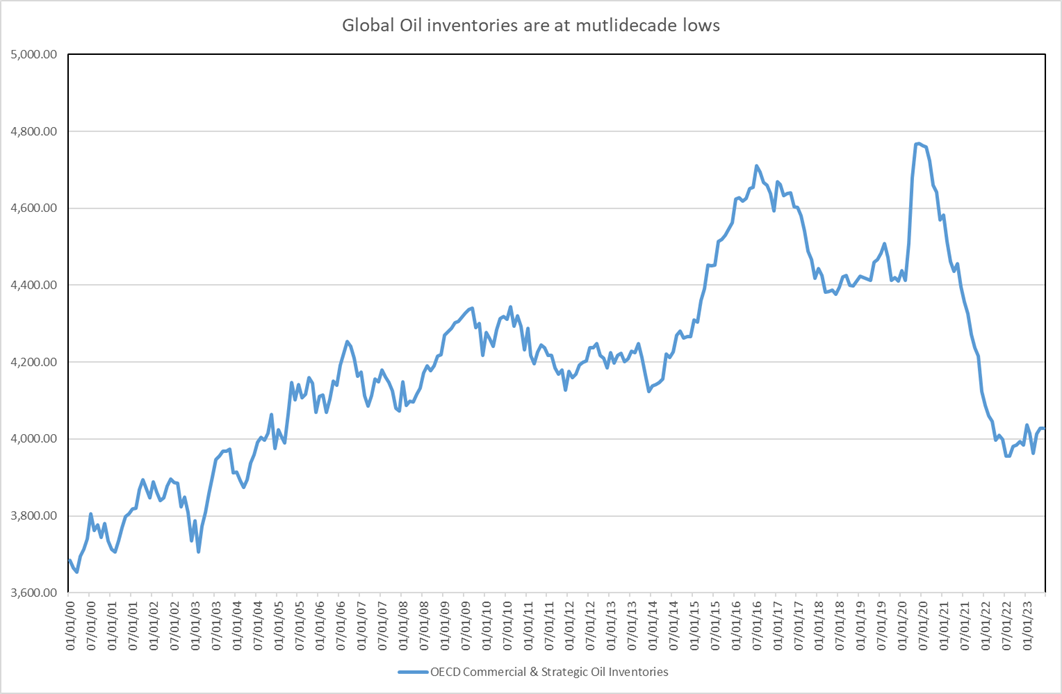

Inflation Protection

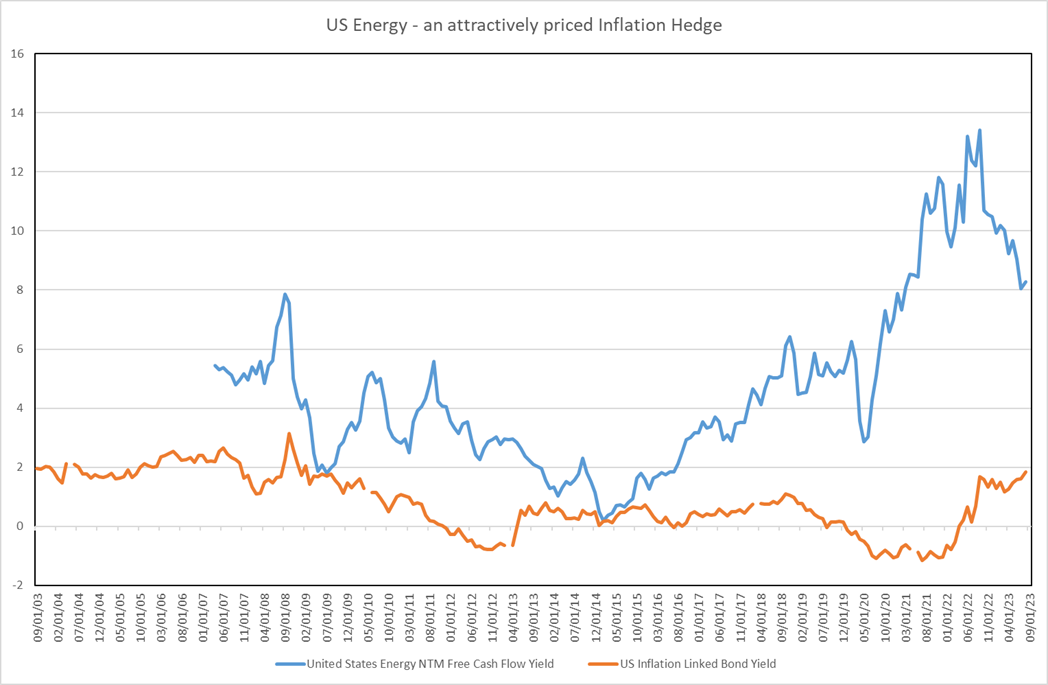

One sector offering strong settings for sustained higher prices is in global energy. In the very long run, these are depleting assets as the ‘Green Transition’ reduces global oil dependency. However, we expect the path to declining oil demand to be gradual at first, as resource and infrastructure bottlenecks limit the pace of the adoption of alternatives outside of Europe, China and, to a lesser extent, the US. For the past decade, underinvestment in traditional oil has already impacted the rate of production outside of the Middle East, while US shale production has narrowed down to a single reserve basin, making for tight energy markets.

Source: Factset Data, Old Mutual Investment Group

Meanwhile, the industry themes for the energy producers look positive. After prioritising growth during the 2012-2020 period, oil companies have shifted focus toward returns. Exploration and capex budgets have been cut, production per employee has increased, and higher margins and free cash flow is being generated per dollar of oil.

Considering the above factors collectively, energy companies appear to be an attractively priced inflation hedge, providing protection against inflationary shocks, and good shareholder returns through sustainably higher free cash flow.

Source: Factset Data, Old Mutual Investment Group

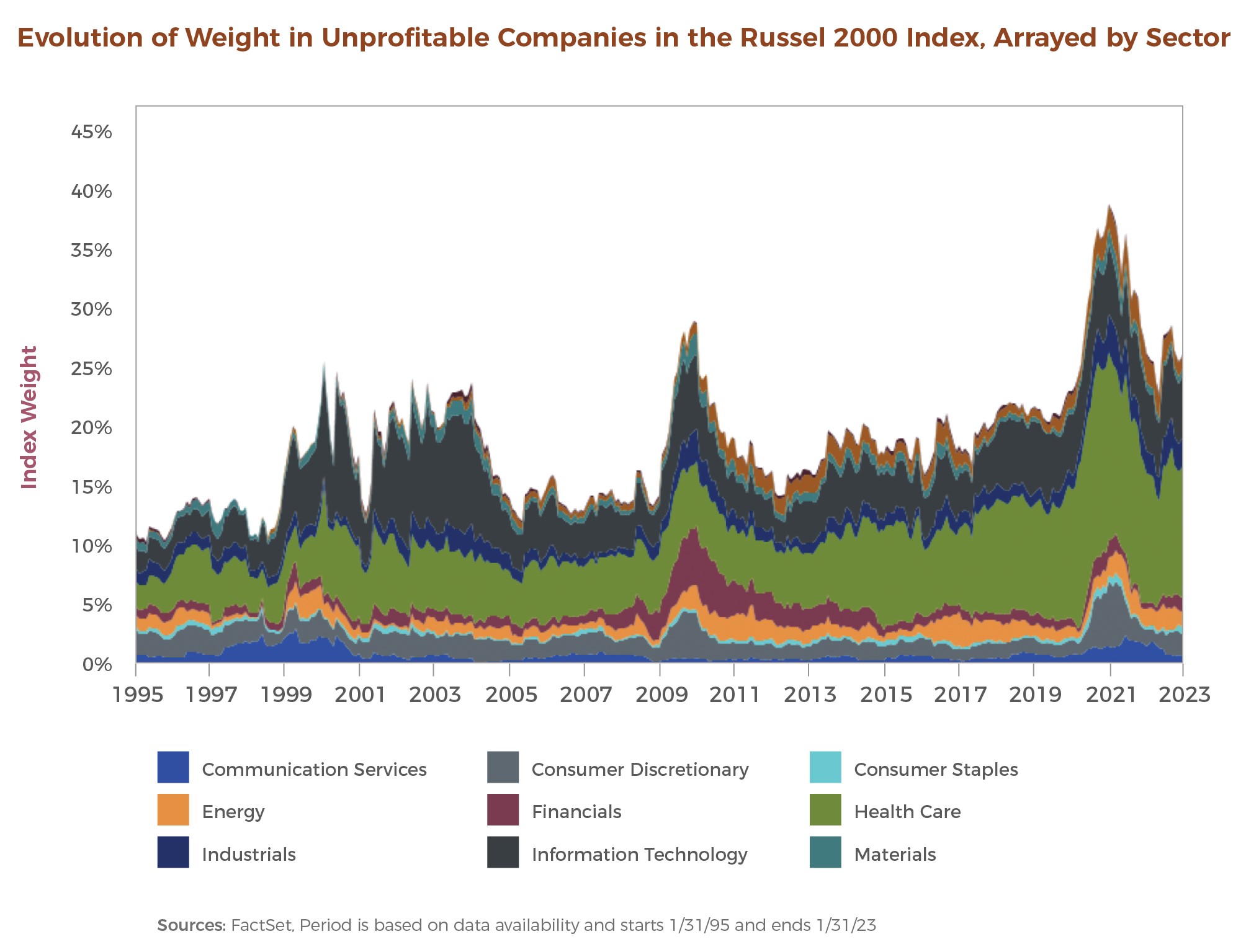

No More Free Lunch

An area we continue to avoid is low-quality growth assets reliant on raising external capital. These companies benefited from free and abundant capital during the zero-interest rate period, allowing them to recycle cheap external cash into long-dated future investments, while current operations were non-profitable.

With higher interest rates, these businesses are forced to either monetise faster, repair balance sheets or attempt to cut costs and investments without sacrificing growth. Some will come out stronger on the other side, but we think the aggregate is likely to deliver poor returns.

Figure 5:

Source: Factset Data

A different investment paradigm

While we have no idea what the level of global inflation will be for the next decade, we are unlikely to return to the low inflation, zero rates world of the 2010’s. This implies a different investment paradigm that will need a different investment approach.

A US and growth centric portfolio would have delivered exceptional returns in the 2010’s, however, the 2020’s will likely require a more balanced global allocation. Diversifying across a broader opportunity set would create a more robust portfolio to navigate the current shifting global themes and increasing risks, which is how we have positioned our portfolio, the Old Mutual Global Macro Equity Fund, in the current environment. DM/BM

By: Zain Wilson, Portfolio Manager, Old Mutual Investment Group