BLACK MONDAY

Platinum group metal sector’s woes get worse after prices plummet

A really bad week for platinum group metals and Chinese property has repercussions for SA’s National Treasury.

What do South Africa’s platinum group metal (PGM) sector, China’s property market and the National Treasury have in common? Well, 14 August may well be remembered as “Black Monday” in South Africa’s PGM sector, when companies saw their share prices tank by as much as 9%.

It was the same day that news emerged that China’s largest private real estate developer, Country Garden, sought to delay payment on a private bond for the first time.

That has serious consequences for the Chinese and hence the global economy and the demand for commodities, including PGMs, at a time when the Asian Tiger is on the prowl for electric vehicles (EVs) that don’t need platinum and its close relations.

The palladium price also tanked that day by more than 3%, extending its losses for the year to more than 30%.

What is the upshot for National Treasury and South Africa’s economy more widely?

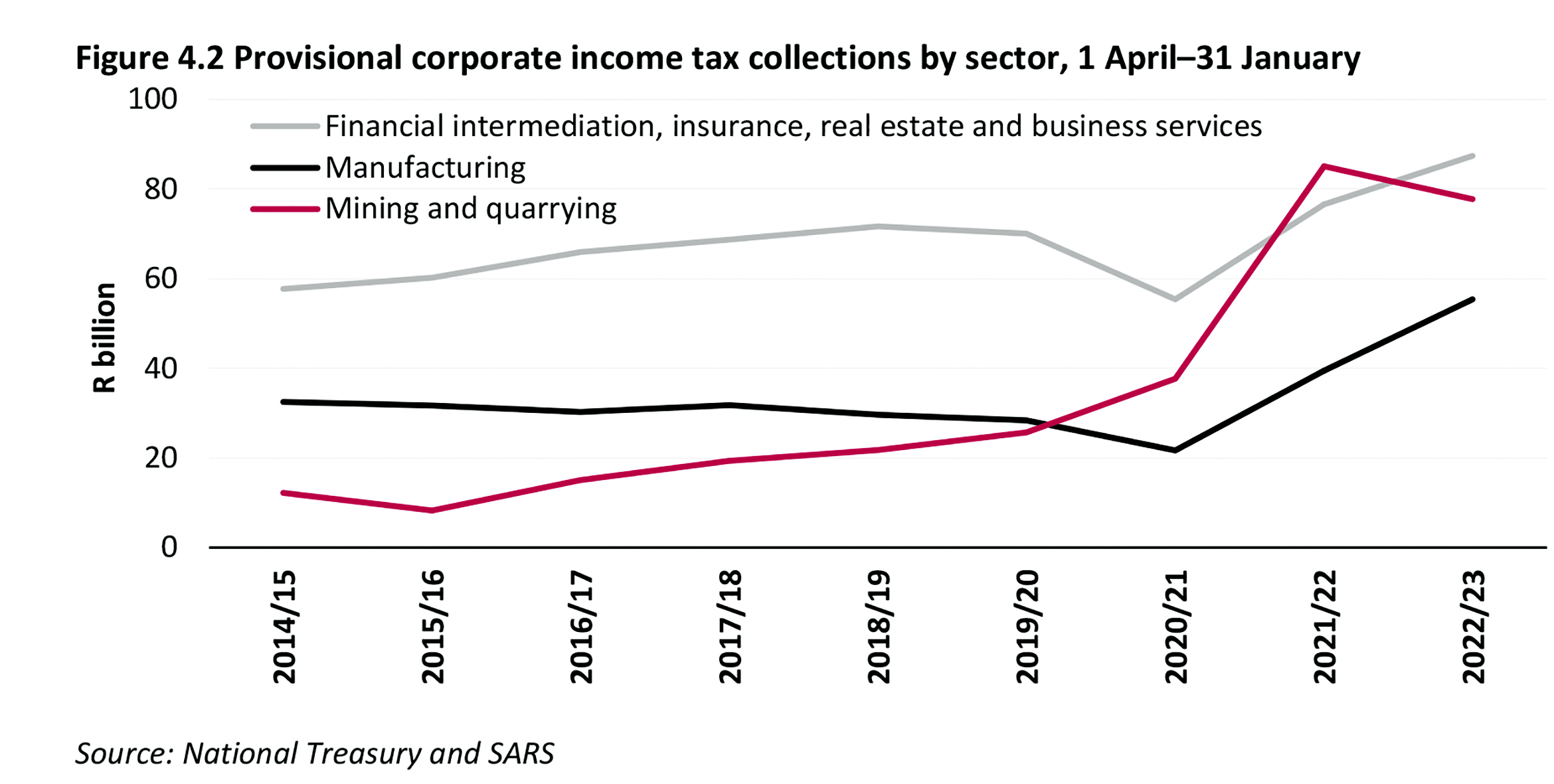

Well, according to Treasury data, as a volume of provisional corporate income taxes paid by three broad sectors — finance, manufacturing and mining — the latter’s share soared from less than R10-billion in 2015/16 to over R80-billion in 2021/22, and was still around R80-billion in 2022/23, when it accounted for nearly 30% of such revenue streams.

“Corporate income tax collections from mining remain large in historical terms due to elevated — although declining — commodity prices,” the Treasury noted when the Budget for this financial year was unveiled in February.

That’s a windfall the Treasury can’t count on this year, when economic growth is expected to slow to perhaps 0.3% from 1.9% in 2022. And PGM prices are a big part of this picture. They are way down, and so the profits and taxes paid by the sector this year will be far less.

To wit, as mentioned, the palladium price is down by more than 30% in the year to date. The rhodium price has fallen by about 65% to just over $4,000 an ounce. In April 2021 it was almost $30,000 an ounce, making it the most valuable precious metal in recorded history. And the platinum price has toppled by almost 16% over the same time period.

This relentless decline has been driven by a number of factors, including slower global economic growth. Things are not as bleak as they were a few months ago, but the International Monetary Fund still projects the post-pandemic global economic expansion to stumble this year to 3% from 3.5% in 2022.

This is not good news for a sector that relies heavily on providing the key ingredients for emissions-capping catalytic converters for internal combustion engines in motor vehicles, a product that requires a robustly growing global economy to pave the road to continued demand — a road already marred by emerging EV potholes.

Platinum can be used in fuel cell EVs, and though growth is seen on this front, in 2022 they accounted for less than 1% of global EV sales.

So, a perfect PGM storm was brewing when the news about China’s Country Garden broke on 14 August.

“Analysts warned that a rise in default by trust companies, also known as shadow banks, which have strong ties to the domestic property sector, will further weigh on the world’s second-largest economy,” a Reuters report said on the day.

Contagion risks

“Anxiety about contagion risks is spreading through global markets, putting China’s government under mounting pressure to deliver support for the ailing real estate sector, which accounts for roughly a quarter of the economy.”

A South African PGM executive told Daily Maverick earlier that the sector was bracing itself for the fallout from the Chinese property market. It appears to have been a catalyst.

And so, on PGM Black Monday, the share prices of major producers tanked, extending already steep declines this year.

The share price of Anglo American Platinum (Amplats) fell by more than 8%, that of Impala Platinum (Implats) by 9%, and Northam Platinum’s by more than 7%. Sibanye-Stillwater’s share price that day dropped by only around 6%, but it has a more diversified production profile that includes gold, a commodity that has fared far better of late.

In the year to date (by 17 August), Amplats’ and Implats’ share prices were down by about 53%, Northam’s was 34% lower and Sibanye’s about 37%.

It is not just PGM producers that have been smacked. Kumba Iron Ore’s share price also took a knock on Black Monday, though it did not fall as far as the PGM producers, yielding 3.4%. China’s property woes and the wider economic consequences that could gush from it will also wash away demand for steel and iron.

Returning to PGMs, Amplats had already produced its interim financial results, which showed a 70% decline in interim earnings.

Northam, in a trading update released on Black Monday, said it expected headline earnings to fall by as much as 12.5% for the year to 30 June, and basic earnings by as much as 80%.

Implats, in a 15 August trading statement, said it expected headline earnings to decrease by as much as 44% for the year and basic earnings by up to 88%. It cited an “18% lower achieved dollar metal price” for the period, and a loss of 147,000 ounces in refined production because of power cuts and cable theft.

There was also an “impairment of property, plant and equipment at Impala Canada of R7.8-billion … due to the combined impact of a material decrease in the US dollar palladium price profile and higher prevailing inflation”, Implats said.

“If the PGM basket price stays where it is until December, most PGM miners will have to cut capex [capital expenditure] to avoid reporting losses,” the mining analyst said.

A cut in capex means less investment that could create jobs or expand production. And if capex gets slashed to keep shafts profitable, job cuts could be next — an unthinkable prospect when producers were posting record profits over the past few years and signing five-year wage deals with unions.

Then there’s the evaporation of the Treasury’s windfall and a decline in export earnings that provide a key base of support for the rand, which has been on the ropes again in August.

The Chinese property market is just one link in this faltering chain, but as PGM Black Monday signalled, it’s one to which markets are hypersensitive. The PGM industry, like other commodity players, needs Chinese growth. And the US subprime market crisis that exploded in 2007 showed just how a property meltdown in a major economy can trigger a chain of catastrophic events.

The PGM market didn’t fare very well in the wake of that. DM

This story first appeared in our weekly Daily Maverick 168 newspaper, which is available countrywide for R29.

Comments - Please login in order to comment.