INVESTMENT PORTFOLIO

Business Maverick’s amateur stock picks for 2023

A team in form - our investments have grown over time, giving us space to explore our options for 2023.

Each year, the Business Maverick team puts heads together to choose the nine stocks they think are worth investing in over the coming year. We are by no means investment experts, but our portfolio remains much stronger than the market, with an overall 18.7% return over two years.

The markets, both local and global, were bleeding almost daily in 2022, across all major asset classes aside from US dollar cash. We invested R180 over two years, with a return of R129.32 at the end of 2021 and a return of R80.73 as at 12 December 2022.

Our 2022 portfolio is down 10.29% year-on-year, which is not good but not terrible. Essentially, we assumed that construction would pick up this year with Aveng in our portfolio. Other than that, we correctly predicted that tourism would come back, but our retail stocks balanced each other out.

Mining and high-end goods seemed like safe bets at the start of the year, and they were, but not enough to compensate for the fact that our construction sector bet was wrong. For the exercise, we assumed an investment of R90, with R10 in each stock.

With stubbornly rising inflation, the Russia-Ukraine war and aggressive interest rate hikes, it does seem as though the bottom has dropped out of the market. However, though this typically leaves most investors wary, there is no better time to find great investment opportunities at low prices.

These are the Business Maverick team’s stock picks for 2023 (share prices at close of day 12 December 2022):

Resources: Exxaro (R221.39) and Thungela (R286.23)

Russia’s invasion of Ukraine not only disrupted financial markets but also led to worries about resource shortages (oil, natural gas and coal). This was not surprising given that Russia provides roughly 10% and 13% of the world’s oil and natural gas, respectively. But coal takes the cup, as it supplies 18% of the world’s consumption.

Since Putin’s temper tantrum that turned into a war, economic sanctions against Russia have forced developed nations to search for alternative suppliers of resources, especially coal. And that search has pointed them to South Africa’s coal producers, such as Exxaro and Thungela.

The share prices of both companies rallied strongly in 2022, shooting up 45% and 228%, respectively.

Western nations are also facing gas shortages and problems with generating electricity from renewable energy sources. This has pushed several EU member states, including France, to extend or reopen coal-fired power stations that were shut down in response to climate change issues.

All of which equals a big demand for coal, driving the price above $400 per ton. Exxaro and Thungela are poised to take advantage of this demand, which will translate into higher earnings and dividend payments to shareholders.

Both companies expect their dividends to grow by at least 12% in 2023, well above the consumer inflation rate of about 7%. The big risk is that Transnet’s port and rail operations might continue to deteriorate, so Exxaro and Thungela might not be able to take advantage of coal export opportunities.

Glencore (R116.03)

This will be a controversial choice for three reasons – Glencore’s continued reliance on coal, the large amounts the company has had to pay to governments this past year because of corruption, and the fact that the share price has already rocketed 150% over the past three years.

Let’s tackle those reasons one by one.

Corruption: the incidents took place a long time ago, in the oil sector, and the company has changed management since then. Hopefully, it is keeping to its word and no more fines will be forthcoming.

But, from a shareholder return perspective, the fines may be depressing the share price and, if the company can avoid a repetition, the market might forgive it and rate the company higher.

Which leads to the second point: the big increase in the share price over the past three years. That means there might not be much upside left. Fortunately, it seems coal prices have not yet been fully integrated into the share price. That is visible from the extraordinary low price-to-earnings ratio of, get this, 4.3. If that is not screaming buy territory, it’s hard to know what is. It’s worth noting that the ratio is more modest than the other big mining companies, even those with significant coal assets.

Finally, how much of a disservice might investors be doing to invest in a company so dominated by coal, from an environmental standpoint? Though, to some extent, this is unavoidable, it’s something of a relief that the company aims to reach net zero by 2050. More than that, it is investing heavily in copper precisely to take advantage of new renewable energy demands. This pick has the potential to really bomb, but, on technical and value grounds, it could also very easily extend its run, particularly if the war in Ukraine continues.

Richemont (R230.42)

The Swiss-based company saw its share price on the JSE fall nearly 4% this year owing to concerns that the share has had a great run since late 2020, as its investment case has become more compelling with strong demand for its luxury brands among upper-income consumers since the easing of Covid-related lockdowns. But the recent decline in the share price arguably creates a cheaper buying opportunity.

Richemont is still generating strong sales in the US and Europe. Although sales in China have been under pressure because of strict Covid lockdowns, Richemont continues to grow in some luxury goods categories, mainly specialist watches.

The company has invested heavily to increase its presence in China’s online shopping industry, partnering with the Alibaba Group to launch a luxury goods platform in this market.

Richemont has a strong balance sheet and experienced leadership (chaired by Johann Rupert) and gives South Africa-based investors Swiss franc-denominated dividends to diversify their income sources.

Precious metals: Sibanye-Stillwater (R48.45) and Anglo American (R682.19)

Sibanye-Stillwater’s share price has plenty of upside room in 2023. As at 12 December, its price-to-earnings ratio was just below 7. The share price was largely unchanged on the year, but was about 35% down on its March peaks, partly as a reflection of prices. However, the price outlook for platinum group metals (PGMs) is upbeat for 2023.

On the gold front, the precious metal’s price has been pinned below $1,800 an ounce of late after scaling more than $2,000 an ounce in March in the wake of Russia’s invasion of Ukraine. Rising interest rates globally have taken some of the shine off gold’s appeal, but central bank purchases hit record highs in 2022 and global uncertainty and geopolitical tensions could enhance gold’s safe haven appeal.

Sibanye’s forecasts are for production costs to decrease significantly.

Vehicle sales are a key driver of demand for PGMs – which are mostly used in emissions-capping catalytic converters – and those are seen picking up some pace as the chip shortage becomes a thing of the past.

Higher PGM prices will also flow to other platinum producers such as Anglo American and its Anglo American Platinum unit.

The company’s diverse offering of commodities should translate into decent earnings in 2023. Goldman Sachs recently raised its forecast for the average copper price in 2023 to $9,750 per tonne from $8,325 as demand is seen rising while supplies remain tight. That should flow directly to Anglo’s bottom line.

The outlook for iron ore, nickel and diamonds is dimmer amid mounting concerns about slowing global growth. Nickel prices remain elevated by historical standards and any turnaround in the Chinese economy as its Covid restrictions relax could reignite iron ore demand.

Sibanye and Anglo may not exactly shoot the lights out next year, but they are both positioned to outperform the wider market by meaningful margins.

Shoprite (R238.98)

This retail stock was one of the star performers in our portfolio in 2022, climbing 14.68%, and we expect no less in the year ahead. Besides being a defensive stock and the country’s largest retailer, management has put significant investment into a digital innovation arm, Shoprite X. This division is responsible for bringing Shoprite’s Xtra Savings rewards and the Checkers Sixty60 delivery programmes to the market. With management bookmarking further investment of at least R1-billion a year in Shoprite X, we are bound to see further digital innovation from this retailer.

Looking ahead, business strategist Jon Cherry of Cherry Flava is convinced Shoprite is setting the benchmark in the retail digital space and cementing its position through partnerships with the likes of Starbucks, Kauai and Krispy Kreme.

“They have purposefully elected to innovate the business by pursuing what is best described as a ‘dual transformation’. Dual transformations happen when the core business is incrementally improved over time, while at the same time riskier new innovations and models are created and brought to market by dedicated but separate business units, which are allowed the space to find their own footing in the marketplace,” he explains.

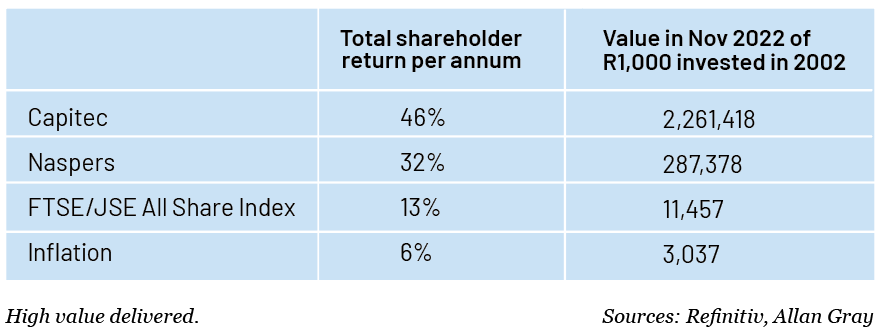

Capitec (R1,871.85)

Once hailed as a challenger bank, Capitec is now firmly entrenched in the banking landscape, carrying the title of the country’s biggest bank with 19 million clients. Having successfully established a firm foothold in the lower-income market, it is now turning its eyes to upper- and middle-income markets. It is also making strides in the rewards space, toppling FNB’s eBucks programme from top spot in the annual South African Loyalty Awards, less than a year after launching its banking rewards programme in March.

Investment analyst at Allan Gray Piet Koornhof notes that Capitec’s management teams have proven adept at managing IT in a cost-effective yet progressive manner as clients migrated from branches to mobile, online and app-based banking.

“Key to this was Capitec’s prioritisation of keeping the client experience very simple and intuitive. Management recognised early on that IT was not just a necessary cost of doing business, but could be a potent competitive advantage,” explains Koornhof.

As reported by Allan Gray in mid-November, if you had invested R1,000 in this stock on the day it listed, your investment would have been worth around R2.3-million last month. Hindsight regret is enough to make one weep.

Naspers (R2,792.07)

A dogged commitment to its ecommerce portfolio – and especially Tencent – and an international, diversified asset portfolio is paying off for investors in Naspers, despite Takealot’s R224-million ($13-million) haircut this past financial year.

A large portion of that growth is owed to the influence of the Chinese ecommerce megalodon, which has been battered by charges of anti-competitive behaviour, President Xi Jinping’s historic third-term re-election and the country’s seemingly endless Covid-Zero lockdowns.

With those now scaled back in response to civil unrest and growing economic woes, China is finally getting closer to a return to normalcy. It can only mean good things for the Chinese stock market and investors in the Johannesburg bourse, given Tencent’s influence via Naspers and Prosus.

Though international ecommerce has been Naspers’s saving grace, in South Africa operations weighed on the company, as the Takealot Group posted a trading loss of almost R224-million in November – despite growing its revenue by 13%.

Last month, Reuters reported that Tencent planned to distribute $20-billion of stock in meal delivery giant Meituan in the new year, which triggered a selloff of Chinese internet stocks as investors feared more divestments by the online gaming company were in the offing.

The government has punished Chinese tech giants for anti-competitive behaviour and the JD and Meituan dividends were likely to be aimed at buying goodwill with the government. In effect, the plan equates to a R100-billion boost for Naspers.

Naspers and Prosus chief executive Bob van Dijk says the companies are adapting to new market realities by preserving liquidity, and taking action to reduce costs and promote free cash flow generation. Tim Cohen, Ed Stoddard, Ray Mahlaka, Neesa Moodley and Georgina Crouth DM168

Disclaimer: This article is intended for consumer education only and is not financial advice. Business Maverick journalists are neither financial advisers, nor do we claim to be.

This story first appeared in our weekly Daily Maverick 168 newspaper, which is available countrywide for R25.

Comments - Please login in order to comment.