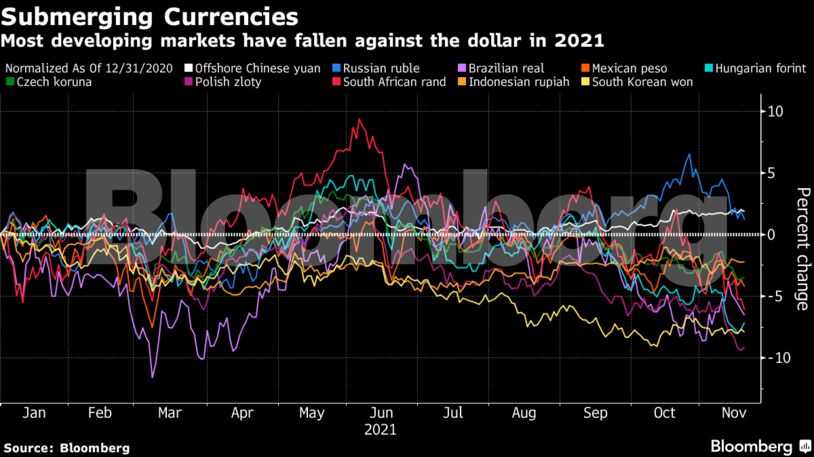

TD Securities reckons that forward markets are pricing in too much weakness for a number of currencies like the real, the Indonesian rupiah and the South African rand, and have recommended a basket trade including these and others.

“With yields adjusting higher, and FX weakening, it is possible that emerging markets will sit better positioned for an eventual Fed rate hike,” TD strategists including Sacha Tihanyi wrote in a report last week. “However, the vulnerability of each EM economy will be important to consider within the context of potential further pressure in 2022.”

From a funding perspective, Latin America appears to be the region most at risk, according to TD, while the outlook for Asia is stronger. That said, strategists see a potential opportunity in Brazil, which is currently being hampered by political uncertainty ahead of elections next year. While there are plenty of risks and potential volatility, they predict the real could restrengthen to the 5 per dollar level, from about 5.57 currently.

Discovery Capital founder Rob Citrone is more circumspect about the prospects for Brazil and Russia. While he sees potential for the real to eventually gain after the noise of the Brazilian election campaign clears, the currency will likely be on the weaker side and markets will remain nervous ahead of the vote. While Russia has seen its currency buoyed by a combination of higher energy prices and rate hikes — and some observers continue to label it as cheap — Citrone says it isn’t worth the geopolitical risk and uncertainty.

For his part, bets on the Hungarian, Czech and Polish currencies against the euro offer the best risk-reward. All three nations have seen central-bank rate hikes and “we think there’s probably some more to go because inflation is higher,” Citrone said. “Despite the rate hikes, the growth prospects for these countries remains much higher. We think all their currencies are incredibly competitive,” he said in an interview.

Here are some of the major events and data to look out for this week:

- Traders will monitor Chilean markets after the Nov. 21 presidential elections, with voters set to either overthrow an economic model installed during the dictatorship of Augusto Pinochet or double down on its free-market ethos

- South Korea’s monetary authority is expected to increase its key rate on Thursday, though investor focus will be more on any clues about the timing of the next hike

- Nigeria’s central bank is set on Tuesday to keep interest rates on hold

- In Mexico, inflation data for the first half of November to be released on Wednesday will probably extend a trend upward, while Bloomberg Economics expects revised third-quarter gross-domestic product figures on Thursday to show a bigger quarter-on-quarter decline than in preliminary numbers

- Mexico’s central bank will post minutes from the November meeting on Thursday, which may offer detail on the odds of a larger interest-rate hike in December

- Data may show that inflation in both Malaysia and Singapore rose in October. Singapore will also release final third-quarter GDP numbers on Tuesday

Comments - Please login in order to comment.