QUANTITATIVE EASING OP-ED

Emerging markets like South Africa will be nervously watching the US Federal Reserve

Investors expect the US Federal Reserve to aim for a fast and tidy tapering of its quantitative easing stimulus measures, with mid-2022 the end goal. But there is little chance of the process happening in a straight line – and those who expect that are naïve.

The moment has come. The US Federal Reserve is set to put its feet on the liquidity brake, slowing down the pace of its bond-buying programme into next year and, so the plan goes, eventually leaving the financial markets to their own devices.

For the past 18 months, its multitrillion dollar stimulus measures have funded the government’s extraordinary fiscal stimulus programmes, putting cheques directly into the hands of individuals and propelling equities to historic highs.

Market consensus is that the central bank is aiming for a “fast and tidy” taper so that it can completely wind down its quantitative easing (QE) measures by mid next year, whereafter it will begin raising interest rates again.

But based on the history of quantitative easing, which is littered with stops, this is, at best, wishful thinking. Despite many attempts to withdraw liquidity from the market in the wake of the Global Financial Crisis (GFC), central banks were still in the throes of it when Covid-19 struck in 2020.

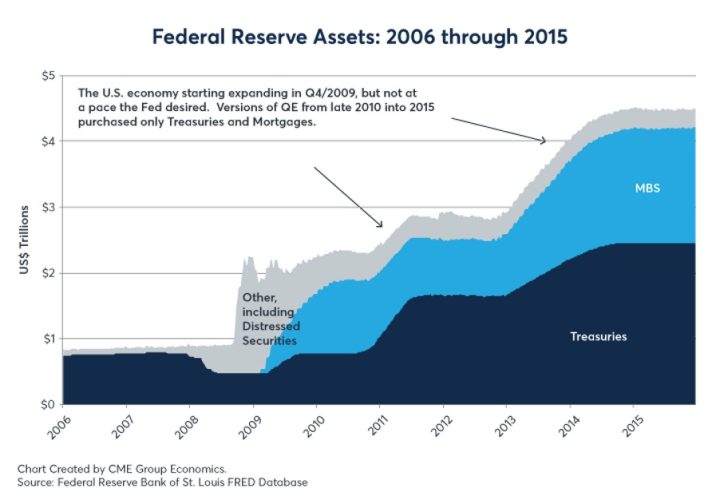

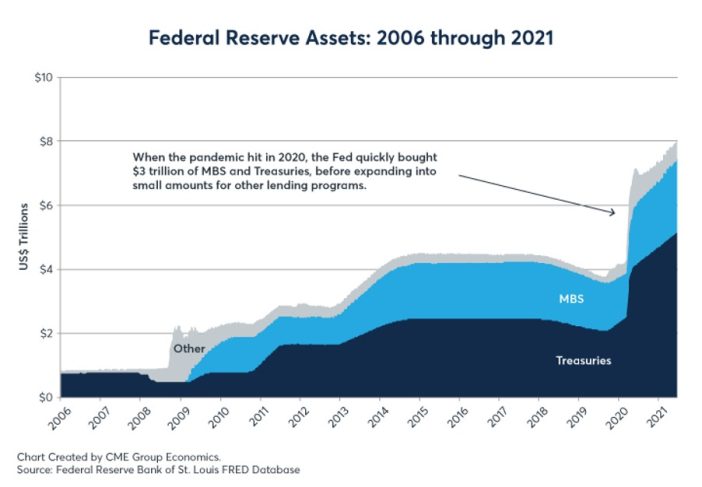

The Federal Reserve’s balance sheet was a hefty $4.5-trillion versus $800,000 before the GFC and before it purchased a further staggering $3-trillion in US Treasury securities and mortgage-backed securities in the weeks after the onset of the pandemic.

There have been several attempts to wind down QE programmes in the US, Europe and the UK since 2007. But within a matter of months, most of these central banks were left with little choice but to continue adding liquidity to anxious financial markets.

For instance, the US announced the end of its first quantitative easing programme in March 2010, only to have to put in place its second quantitative easing (QE2) programme less than six months later. QE3 came into being in September 2012. In May 2013, the Fed felt the full force of the market’s discontent, in what was referred to as the 2013 taper tantrum, after Fed chair Ben Bernanke announced his intention to slow down bond purchases.

Against this backdrop, it’s naïve to expect the Fed’s tapering programme, no matter how carefully and well telegraphed it is to the markets by Powell, to be neat and tidy. The world economy is still in unprecedented territory, the financial markets have been on life support for a decade and a half, and the new normal is nowhere in sight.

It’s also uncharted territory for central banks that may have been engaging in quantitative easing for 15 years but for very different reasons. The QE programme initiated to support economies hit by the pandemic is significantly different to the QE programmes that took place between 2007 and mid-2019. The key difference is that the current programme is facilitating direct payments to individuals and businesses via the government’s debt-funded stimulus programmes, whereas the previous rounds of GFC-related QE programmes bought distressed debt and never provided direct assistance to individuals.

Thus the entirely different nature of the previous QE programmes compared with the current one in play means that the Fed’s actions and impact on financial markets over the next 18 months are likely to be anything but predictable.

That is evident in particularly nervy bond and emerging markets ahead of the Fed’s announcement about the potential pace of withdrawal of monetary policy stimulus. Stock market investors, in contrast, remained remarkably sanguine, still buoyed by an overwhelmingly positive third quarter earnings season.

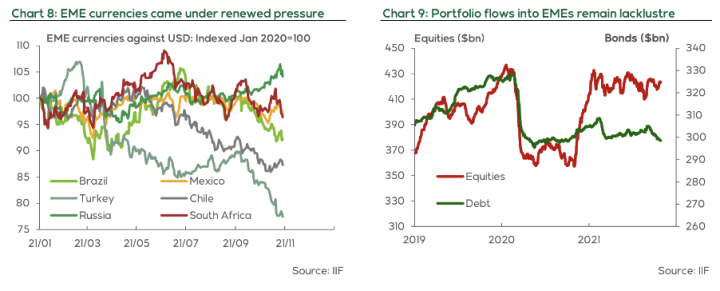

The success – or lack of it – of the Fed’s QE actions over the next few years will have significant ramifications for emerging markets like South Africa, because they will bear the brunt of any volatility that stems from developed country financial markets. We have already seen early signs of this in the lacklustre portfolio flows into emerging markets during September and October, as recorded by the Institute for International Finance (see chart 9 below). The South African rand has weakened and economists expect it to continue to lose ground in an environment of more hawkish global monetary policy.

Investec economist Annabel Bishop points out that the rand depreciated to almost R15.50 to the dollar ahead of the US Federal Open Market Committee meeting outcome. In contrast, oil-exporting emerging markets like Russia experienced currency gains (see chart 8 below). Other countries with stronger emerging market currencies have been those that have lifted their interest rates in recent months.

Nedbank’s economic team, referring to the rand wobbling as central banks have become hawkish, confirms that on average, the currencies of countries that hiked interest rates quite aggressively in response to rising inflation and the upcoming tapering of US bond purchases have “fared somewhat better than those that either moved slowly or kept interest rates unchanged”. South Africa fits into the latter camp.

Bishop says negatives for the rand this year would be a reduction in the dovishness of the US Fed, as reflected by their intention to begin tapering, and marked worries about inflation.

Nedbank economists are also not optimistic about the rand’s prospects this year and next, expecting the currency to depreciate for the rest of the year and to exhibit “significant weakness” next year.

“Global risk sentiment will probably become even more volatile, sensitive to the threat posed by a mutating virus, higher inflation and the shifts in international monetary policies. These uncertainties are likely to subdue risk appetites for emerging market assets, weighing on the rand. Commodity prospects also appear murkier as China faces more significant downside risks from the weakness in its property market and the drive to shift its economy towards higher value-added manufacturing and services.”

With so many unparalleled economic cross-currents at play, it’s hard not to feel trepidation ahead of the US Fed beginning to unwind its massive balance sheet – whether that happens now or next year. The only real option we have is to buckle up and prepare for the ride of a lifetime. DM/BM

Comments - Please login in order to comment.