BUSINESS MAVERICK: OP–ED

The MTBPS: Much worse than expected

The mini-budget tabled in Parliament last week is a wake-up call. It shows unequivocally that the path South Africa is on is unsustainable: debt is rising, growth is falling, and there is no real plan to get the government’s finances under control. ‘Hope’, as Finance Minister Tito Mboweni said, ‘is not a strategy.’ Until there is one, however, the risks that our public finances pose to the country’s future prosperity are enormous.

By far the most shocking piece of data in the mini-budget tabled by the Minister of Finance shows the extent to which previous estimates of the sustainability of SA’s fiscal policy actually understated the severity of the crisis. Analysts and financial markets were genuinely surprised by the extent to which the Treasury itself now estimates that our fiscal position has deteriorated.

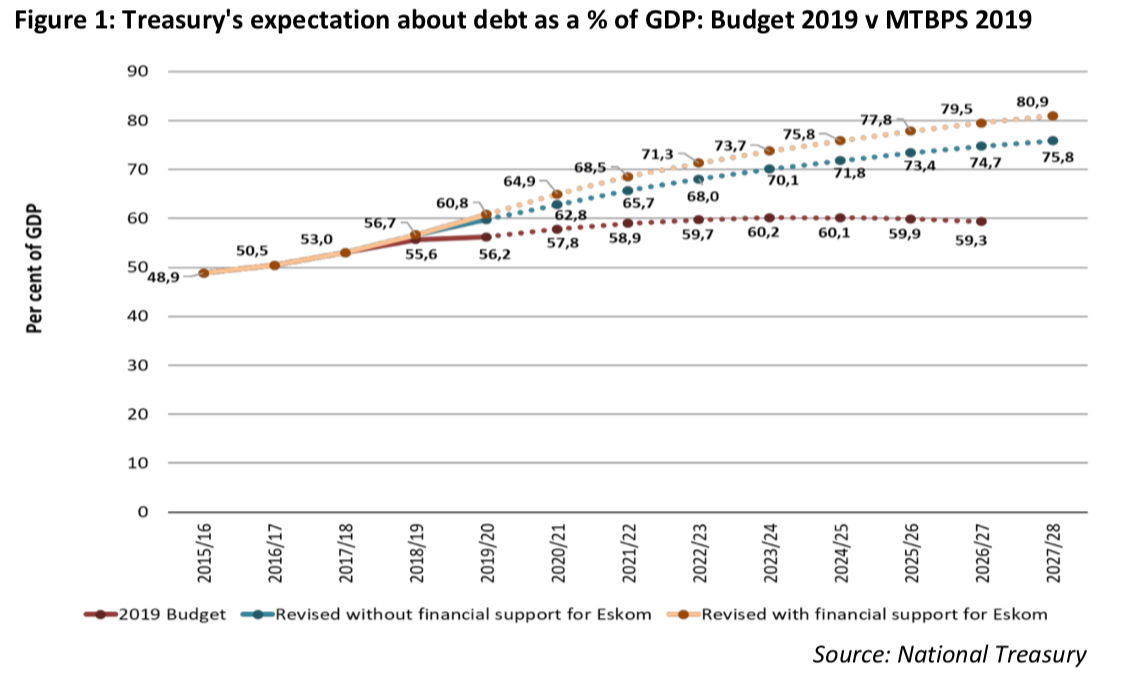

This is reflected in the figure below, which shows the path of debt to GDP projected in February (the red line) and compares it to what Treasury now expects to happen. The first line (published just eight months ago) projects debt stabilising at about 60% of GDP in 2023; the new calculations show:

- that debt will be much higher in 2023, and

- that it will continue to grow in relation to GDP until at least 2027, by which point it will have hit 81% of GDP. Given that the equivalent figure was 30% in 2008, the collapse of our macroeconomic fundamentals is truly astonishing. These figures, it should be said, exclude the debt of state-owned companies (SoCs), which would add as much as 10 to 15 percentage points on to these estimates.

There are four major reasons why the picture seems so much worse now than it did in February 2019:

- Treasury’s assumptions about the rate of economic growth are much lower than they were (0.5% in 2019 compared to 1.5% in the February budget, for example, with expected inflation also lower), implying that tax collection will also be lower;

- The extent of the underperformance at SARS means there is even more revenue under-collection than previously anticipated (reflected in lower estimated revenue buoyancy – which is the percentage increase in tax divided by the rate of growth of the economy);

- The SOCs, Eskom in particular, are now expected to need even more support from the fiscus than had been anticipated in February (with some of that additional assistance already having been made available through an additional appropriation last month);

- Despite these impending revenue shortfalls, nothing very significant has been achieved by way of reducing spending, with barely R50-billion in cuts pencilled in for the next two years.

Revenue growth is collapsing

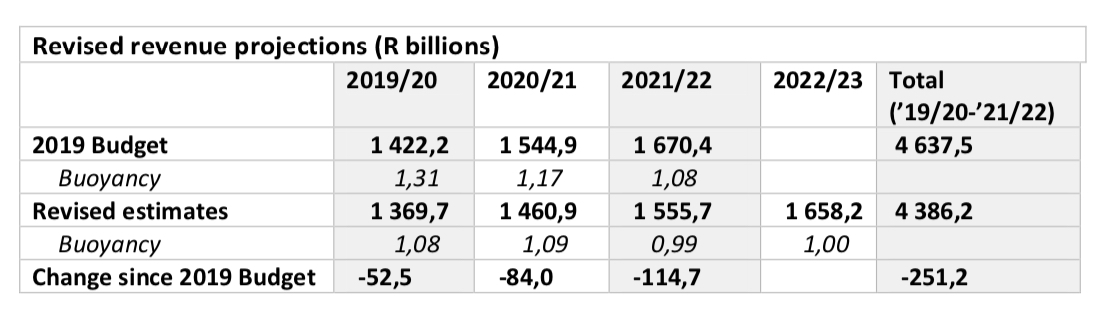

The size of the anticipated shortfalls in revenue is reflected in a table published in the MTBPS. It shows that Treasury is now expecting to take in a total of more than R250-billion less revenue in this financial year and the next two than it had expected to do in February. This is because revenue buoyancy is expected to be much lower (1.08 in 2019/20 compared to a hoped-for 1.31) and because nominal GDP growth is slower (because expected inflation is falling and the rate of growth is, too). Slower nominal GDP growth explains about 60% of the decline in revenue projections, while lower levels of revenue buoyancy explain the rest.

The impact of the lowering of assumptions about both growth and revenue buoyancy that underpin the fiscal framework has two very significant effects on the ratio of debt to GDP. First, it means that, unless spending is also cut, the decline in revenues must imply larger borrowings. Second, because the economy is growing more slowly, the ratio in relation to GDP of any given amount of debt rises. These two factors are the drivers of the exceptionally rapid increase in the level of debt-to-GDP predicted in the MTBPS relative to what was projected in February. This is critical because it shows – once again – that the road to fiscal sustainability runs through policies that would accelerate economic growth.

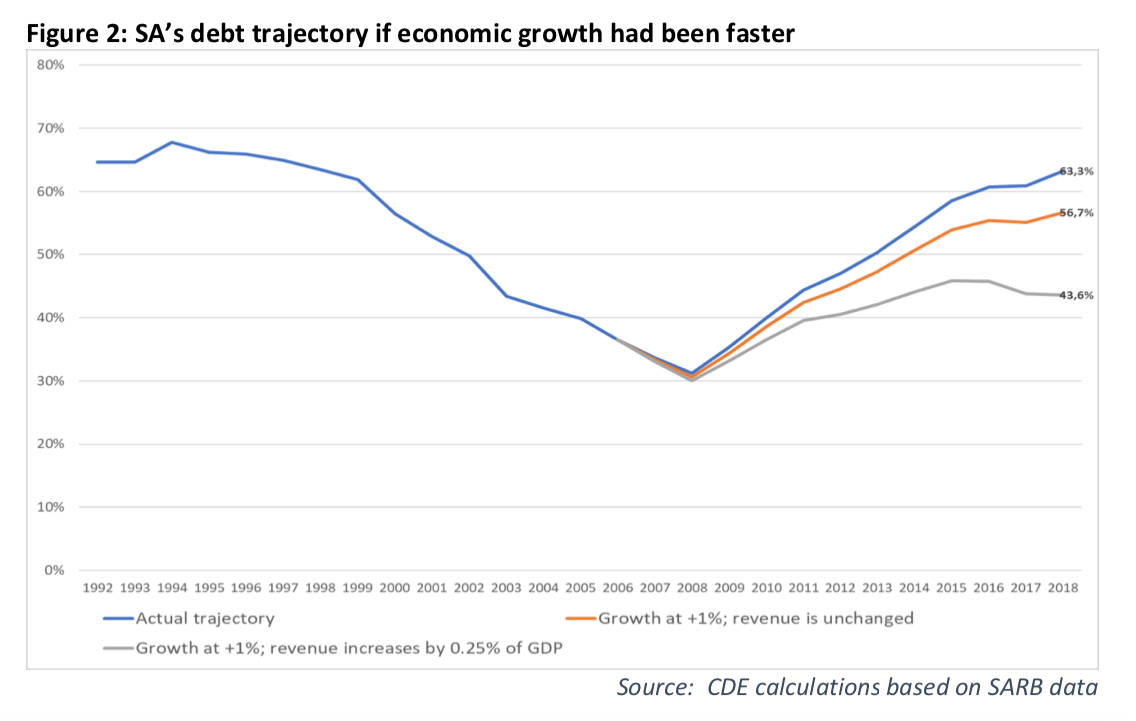

This is a point that CDE made in our report on fiscal policy released in August 2019, Running out of Road (see here), even a one-percentage-point a year increase in growth would have profound implications for fiscal sustainability. Using data available then, we showed that if growth had been one percentage point higher than it was in every year after the 2008 global recession, in 2018 SA’s public debt (including the SoCs) would have been 44% of GDP and falling rather than 63% and rising.

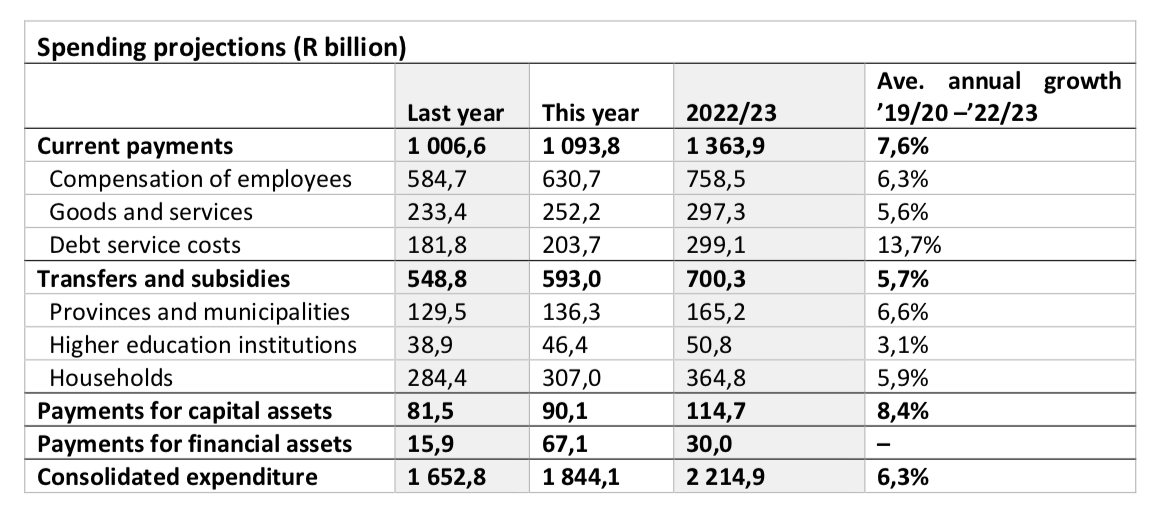

The growth of public spending is not falling

Although it is the slowdown in economic growth together with the even more rapid slowdown in expected tax revenue growth that drives the deterioration of our fiscal position, the absence of meaningful reductions in the rate of growth of public spending also plays a critical role.

As can be seen from the published spending plans, Treasury is currently expecting that spending will grow from R1.8-trillion in 2019/20 to R2.2-trillion in 2022/23, a rate of increase that averages 6.3% a year. This is fairly rapid growth when inflation is expected to be around 4.5% a year and economic growth is below 1 per cent a year (although Treasury expects this to pick up modestly, to 1.7 per cent in 2022/23). This is not a plan for fiscal consolidation led by spending restraint, which is what CDE called for in Running out of Road.

Apart from the relatively rapid rate of spending growth in the aggregate, a couple of other points are worth noting:

- Debt service costs rise from R182-billion in 2018/19 to R299-billion in 2022/23, at a staggering rate of nearly 14% per year.

- There is no restraint in compensation spending, which grows at 6.3% a year.

- There is a real squeeze on higher education, the budgets for which will grow at only 3.1% a year.

- Transfers to households – which includes both social grants and housing subsidies – grow less quickly than spending overall.

Provisions for “payments for financial assets”, which is driven by loans and equity injections into SoCs and has frequently been zero, amount to over R200-billion across the current year and the next three.

The minister of finance has himself described government’s spending plans as unsustainable and expressed the hope/intention to present a budget in February 2020 in which savings totalling R150-billion have been stripped out of these spending guidelines. It is clear, however, that he has not yet been able to secure Cabinet’s full backing for doing this; if he had, he would surely have presented a very different mini-budget.

It cannot be stressed too strongly that unless such cuts can be effected, South Africa’s creditworthiness will plummet further and we will be faced with even higher borrowing costs – both in the public and private sectors. And, as a result of that, we will see even slower economic growth. Thus, even as the road to fiscal sustainability passes through the policy reforms needed to achieve faster growth, the road to faster growth passes through meaningful fiscal consolidation that de-risks the economy and lowers the cost of capital.

The pressing need for faster economic growth

While spending growth must be restrained, and some of the burden of this will have to fall on the public sector salary bill, there is very little chance that this can bear the full weight of adjustment. Overly high though it is, we cannot realistically expect public spending to fall very much in the short and even medium terms. This would be hard to achieve in a stable, wealthy democracy; it is impossible in a society shaped overwhelmingly by its inequalities and in which politics are as fraught and dangerous as are ours.

Given this, we absolutely have to see growth-accelerating reforms. Everybody knows this already, what has been lacking is the will to make the decisions that are needed, and which, in the nature of things, will mean that those who benefit from existing policies will have to be confronted. The costs of failing to act are high and mounting. Leadership is required now to define the national interest and implement appropriate reforms.

What kinds of policies do we need to raise our chances of growth?

- For the reasons outlined above, meaningful fiscal consolidation;

- A determined programme of institutional reform, business restructuring and market liberalisation in a range of economic activities currently dominated by badly run SoCs that destroy far more value than they create, chief among them electricity generation and distribution;

- A determined focus on improving the regulatory environment that stifles business formation and growth, with a particular focus on:

- Addressing the unnecessary costs and perverse incentives associated with complying with existing transformation-focused legislation;

- Improving regulatory processes associated with registering businesses, paying taxes (and receiving refunds). Obtaining building approvals.

- Addressing immediate skills constraints by opening up the migration regime for skilled immigrants coupled with energetic efforts to recruit as many skilled people as SA can attract; and

- Implementing sector-specific reforms that have the potential for significant impact, including:

- A much more liberal visa regime for tourism;

- The sale of the spectrum;

- Recrafting the Mining Charter.

The government needs to implement these vital reforms and its actions, implementation and communications need to reflect a real sense of urgency.

Given the bleakness of the picture painted by Mr Mboweni last week, the decision by Moody’s to immediately reset the outlook of our sovereign rating to negative was entirely understandable. It is doubtful the minister had any expectation of any other outcome. The critical thing now is to act: everyone knows what has to happen to accelerate fiscal consolidation and improve the growth outlook, but knowing and doing are two different things.

The government must now act. To do otherwise is malpractice and risks condemning the country to declining real per capita incomes and increasing unemployment for a very extended period. No government can survive that for long, so it is in all of our interests that, however hard the political challenges appear, the government tackles them decisively. And soon. BM

Bernstein is the CEO of the Centre for Development and Enterprise. The analysis was produced by the CDE.